Source: Euronews

Digital currencies have grown in popularity. Unlike bitcoin, the digital euro would be a central bank digital currency (CBDC), essentially, electronic cash. The aim is to offer consumers an alternative Europe-wide payment option.

Are Europeans ready to introduce a digital version of the euro? After coins and banknotes, the European Commission is now proposing the digital euro, a virtual version of the currency issued by the European Central Bank that could be used free of charge alongside cash in the eurozone.

Why do we need a digital euro?

How would European citizens benefit from a digital currency and what approach should be taken to develop it? The Commissioner for Financial Services, Financial Stability and Capital Markets Union, Mairead McGuinness, explained the challenges of creating this new currency and why we need a digital euro:

"It's such a new concept. People are wondering. So this is the euro, it’s cash. And you know what, you see it, you understand it, but maybe I won't have cash in my pocket. So I want the alternative, the choice to have a digital version of cash. People aren't using cash as much as they used to, and COVID-19 accelerated that trend. So it's about choice, essentially. Will I use this cash, which isn't in my wallet today, but it normally is? Or will I use a digital version of cash?"

Overview of the digital euro

The digital euro will be a digital version of euro notes and coins. It will have the same value and can be used in the same ways: To buy ice cream or clothes or to send money for a birthday party - even across national borders.

You could e.g. For example, use a QR code to make a payment from a secure app on your phone, and even make payments when there's no internet connection.

When fully deployed, merchants will need to accept the digital euro the same way they accept cash today.

The digital euro differs from cryptocurrencies as the European Central Bank backs it and thus its stability is guaranteed.

In a digitized world, the digital euro aims to enable everyone to make secure payments, anywhere in the eurozone.

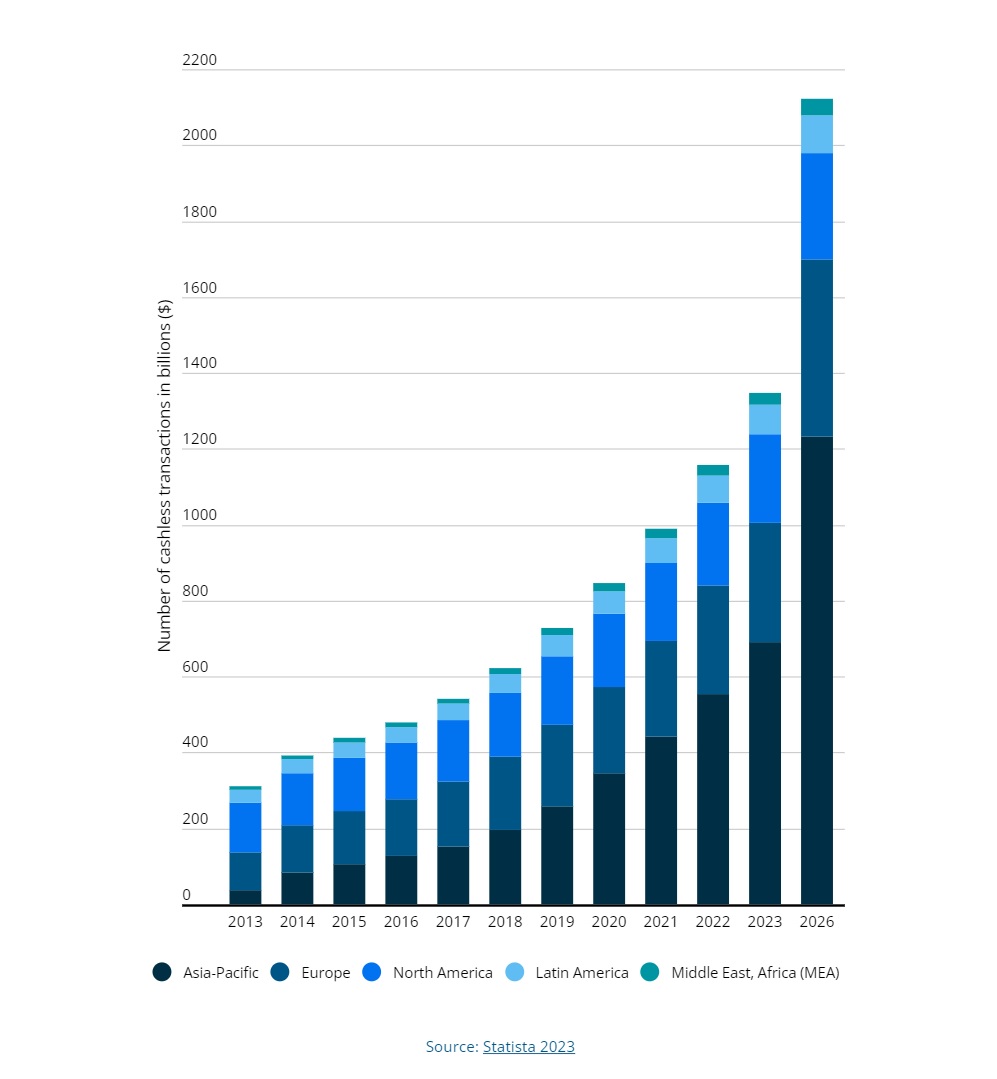

Number of cashless transactions worldwide

From 2013 to 2021, with forecasts from 2022 to 2026

Credit and debit cards, direct debits, and credit transfers remain the most popular electronic payment methods. However, there are also other types of mobile payments, such as e-Wallets, although these depend to a large extent on existing processes.

When asked what advantages the digital euro would bring to EU citizens, the EU Commissioner replied:

"When we try to get our minds around a digital euro, so this is a wallet and I have euro cash in this wallet as well. But I'm like, I don't want to break my €50 because I have it for something else. So I might decide to use the digital wallet to pay for the euros, for these drinks. So cash is how people might pay today, but more and more, they're using cards or their phones. And we want to have the option of the cash equivalent in digital format. And now we've proposed legislation, but that's only the start of a process".

The difference to a cashless, contactless payment is "It is different because it is central bank money, whereas the other payments are private money. You know what its value is. And therefore we want to translate that same sense into the digital era because more and more we are using digital payments."

Will cash go away?

The central banks are concerned that the digitization of payments might unroot the anchor that cash brings to their financial systems. A digital equivalent of cash would help support the sovereignty and stability of this system. Euronews spoke to economist Maria Demertzis, a senior fellow from the European think tank Bruegel, in the museum of the National Bank of Belgium.

"It's interesting how cash develops," Demertzis said. "After the pandemic, we thought that most of the payments were done digitally. But, if you look at the numbers, these are ECB numbers, 42% of the value of all transactions in the euro area in 2022 were done in cash. 42% is not quite half, but is very, very close to being half. I think that the direction of travel is a reduction of cash into more digital payments, but I do not think that it will disappear."

How would the digital euro be designed?

Maria Demertzis said: "When it comes to our everyday payments, which are not going to be very different, it's probably going to be an app. It will probably be intermediated by financial intermediaries like banks and it will be paid in the shops and just like we pay digitally with any other means. And given that at least at the beginning, the ECB will only start with small amounts, we will not be able to have more than €3000 or €4000 in the bank, it will not make much of a difference to the consumer.

"If you want the digital euro to mimic cash as much as possible, you need to make an effort to make it as anonymous as possible. And here, the ECB is telling us that there will be anonymity for small levels of payments. But as you start paying bigger amounts of money, it will no longer be anonymous." she added.

The European Central Bank conducted a public consultation on the digital euro. The concerns that emerged from it were privacy (43%), which was the highest percentage, followed by security (18%), usability across the Eurozone (11%), absence of additional fees (9%), and offline usability (8%).

Data protection associations also raise concerns about privacy, anonymity, and payment tracking.

Commissioner Mairead McGuinness is right to question who is monitoring spending when using the digital euro but said: "The ECB is not interested in how you spend your money, but they want to give you the option of having a digital version of cash. So you can use a digital euro payment offline. If you use your digital wallet offline, it's a private transaction. Of course, if you're doing an e-commerce transaction, your bank will know that you're using your digital euros to do that. But I want us to have these conversations so that people if they are concerned, we can answer those questions and put their minds at ease."

Opportunity for the economy

Despite the privacy concerns, the digital euro represents a commercial opportunity, especially for FinTech companies, as Jan Boehm explained: "Fintechs are young companies, technology companies that provide financial services. We are very innovation-driven. We are technology oriented, and we provide solutions for clients such as, for example, this payment solution, that you've just used when you've paid for your coffee.

Future users could benefit from these innovative services, initially private individuals and companies in the euro area.

"Today, the European payment landscape is very fragmented. So we have several US firms that provide card payment schemes and people use Paypal, for example, for peer-to-peer payments. But we don't have a European system so much. The role of fintech is obviously to provide innovation but also to provide disruption for greater transparency which should result in better products for clients, also, lower fees" said Boehm.

Around 120 central banks around the world are currently working on digital versions of their national currencies. The European Commission's proposal for the digital euro outlined on the 28th of June aims to create the legal framework for this; a common proposal that ensures the preservation of the cash.

When is the digital euro coming?

The Commissioner explained the following steps: "Well, this will not be my decision. The legislation is to put, if you like, democracy in action around a digital euro, and that process is up to the European Parliament and Council. So the ECB will decide if and when a digital euro will be launched and there is no date on that".

Special thanks to ‘PIM coffee on the go’ and ‘Brasserie Byblos 1898’, where this episode was filmed.